|

Download this letter as a PDF!

May 20, 2022

Dear Chairman Ghaly and Commissioners,

Thank you for the opportunity to provide public comments to the Healthy California for All Commission on the Final Report, Key Design Considerations for a Unified Health Care Financing System in California.

Licensed health insurance agents help millions of Californians find and utilize affordable health care coverage, reducing the percentages of those who are uninsured to record lows. Through this work, agents are intimately aware of the importance of health coverage and affordability of that coverage. California Agents & Health Insurance Professionals (CAHIP) previously the California Association of Health Underwriters (CAHU) is the state’s largest association of health insurance agents, brokers, and other health insurance industry professionals.

CAHIP shares the Commission’s objective to ensure that all Californians have access to high quality, affordable healthcare and to improve transparency and stability in pricing. While we have strong concerns with some of the proposals that have been put forward, our comments focus on viable market stabilization strategies that will help California continue to lead the nation in successfully administering the Affordable Care Act (ACA) and achieving universal coverage. To that effect, we offer the following six considerations on the proposed stages to “Lay the Foundation” for California’s path to Unified Financing:

1. Fortify the Public Health System

Support Efforts to Fix the ACA “Family Glitch” and Extend ARPA

Independent agents are an important driver of Covered California’s success. Half of all consumers enrolling in Covered California do so through independent agents. Agents are the faces of Covered California and year after year are the largest and customer-preferred source of enrollment. As the individuals that have been working hard to make the California Exchange the most successful marketplace in the nation, agents know firsthand what works and what can be improved.

A weak spot within the current ACA structure is commonly referred to by agents as the “family glitch.” The ACA guarantees “affordable coverage” but affordable coverage is not yet a reality for everyone. The “glitch” occurs when an employer pays for health coverage for their employee, but not for the employee’s dependents. This glitch happens often when small business employers, who are not required to provide health benefits, choose to offer health insurance to their employees, based on what they can afford. Currently, because a member of the household (the employee) is offered affordable health insurance through their employer, the glitch will not allow spouses and dependents access to ACA subsidies. This gap increases the number of uninsured, especially among children. In instances where coverage is not extended to dependents in employer-based coverage, the family should not be denied “affordable coverage” in the form of premium assistance that they need.

The Biden Administration recently announced that it would release a proposed rule to fix the family glitch. This proposed rule is a result of President Biden’s Executive Order from 2021 calling on the federal agencies to strengthen the Affordable Care Act. The Department of Treasury is using the proposed rule to revise the definition of "affordability" of employer sponsored coverage as it applies specifically to family members of the employee. Under the proposal, the earliest this change would be enacted would be January 1, 2023. We encourage elected officials and regulatory experts in California to support the proposed rule change currently in the rulemaking process.

The ACA can be strengthened by permanently extending the American Rescue Plan Act of 2021 (ARPA), which substantially improved affordability through enhanced premium assistance for 2021 and 2022. ARPA also limited consumer’s required contribution to no more than 8.5% of household income, which means that more individuals and families are eligible for more financial help. Extending ARPA subsidies and fixing the “Family Glitch” would help California move closer to the goal of affordable universal coverage.

Close the Uninsured Gap

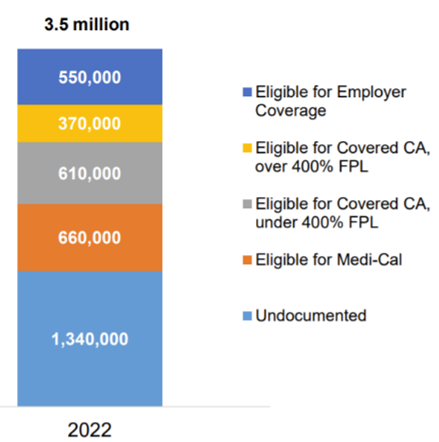

Using UCLA-UC Berkeley CalSIM data, the first Commission report projected that in 2022 there would be 3.5 million uninsured Californians. Per the Figure below, other than individuals that would be eligible for other coverage sources (through the exchange or their employer), undocumented Californians make up the remaining uninsured. Under AB 133, California recently became the first state in the nation to expand full-scope Medi-Cal eligibility to low-income adults 50 years of age or older, regardless of immigration status. This was a major milestone in the state’s progress toward universal health coverage, and approximately 235,000 Californians aged 50 years and older are newly eligible for Medi-Cal. Combined with legislation from 2019, California also extends Medi-Cal coverage to all eligible undocumented young adults up to the age of 26.

The Governor’s most recent budget proposal would close the existing age gap of 27-49 and give an additional 700,000 undocumented Californians access to health insurance. The expansion would make California the most inclusive state for health coverage in the country and the first to achieve universal access to healthcare coverage.

FIGURE 1

2. Implement Cost Containment Measures

Health Insurance Costs are Contained Through the Existing Medical Loss Ratio

It is important that Commissioners and stakeholders become familiar with the minimum medical loss ratio (MLR) percentages established by the ACA in 2011 that are currently applicable to health care service plans and health insurers in California. For all individual and group health plans, at least 80% of the premium dollar must be spent on direct patient care. For large groups with at least 100 employees, at least 85% of the premium dollar must be spent on direct patient care. The remaining 15%-20% is used for overhead costs, such as administrative costs, sales expenses, and profits. Health plans and health insurers annually submit their ratios of incurred losses to earned premiums, or MLRs, to the federal Department of Health and Human Services (DHHS).

Existing law also requires a health care service plan or health insurer to provide an annual rebate to each enrollee or insured under their coverage, on a pro-rata basis, if the MLR is not met. Decreases in the minimum MLR have been attempted in legislation (AB 2499, Arambula, 2019), but were ultimately found to limit the incentives to reduce medical costs, and ultimately contribute to higher medical cost and premium trends. This is because the only way to increase margins with an MLR minimum is to allow claims to trend upward, so that premiums grow, and the allowed administration and profit percentages can be based on a larger number. As a result of lower MLRs, carriers may also limit spending on cost containment measures like network management, quality and outcome analyses, provider negotiations, and fraud waste and abuse studies, or exit the California market entirely.

Further, carriers with higher MLRs should not necessarily be considered more efficient; often they have simply done less to reduce medical cost trends, which have continued to outpace non-medical consumer price inflation by a wide margin despite the federal MLR floors. If MLRs are set too high, carriers will simply leave the market. Accordingly, agents are concerned that related efforts would cause those currently insured in the large group and individual markets to lose their health care coverage if their plan is forced to exit the market.

Alternative Pricing Models

With consideration that some providers may leave practice in California if they are required to work for a particular wage, further exasperating an existing shortage of providers, CAHIP proposes that the Commission not set the price that doctors and facilities can be paid. Instead, we recommend you gather information on pricing, and suggest a price that would be deemed fair. This would be comparable to the example of the automobile manufacturer’s suggested retail price (MSRP). This suggested price would provide significant pricing clarity for both consumers and plans when negotiating fair and appropriate payment.

We propose that the Commission require all doctors and facilities to use Medicare pricing as the reference point when they bill for services. There would be flexibility to charge rates that account for regional needs and specialty skills, but they would have to indicate what that price is compared to what Medicare pays. This reference-based pricing (RBP) has become widely used in the self-insured market and has reduced costs substantially. Self-insured RBP plans use a stated percentage above Medicare rates, such as 200% of the Medicare rate, when paying providers. This is a consistent and cost-effective referenced rate that is widely accepted and easy to understand.

For example: Hospital A charges $75,000 for a hip replacement which is 250% of what Medicare pays and Hospital B (a research hospital) charges $150,000 for the same procedure, which is 500% of what Medicare pays, but has significantly better outcomes in more complex cases. This would allow for consideration of specialties that have outcomes that may warrant a higher cost. This model allows providers to charge rates that appropriately reflect their expertise, while still providing consumers with appropriate price disclosures that allow them to make informed decisions about their care. This method could also be used to provide incentives for providers to serve underserved communities. The state could commit to higher percentages of reimbursement to fund quality care in facilities with providers serving Californians with the greatest needs.

CAHIP appreciates the Commission’s consideration of a model based on the success that Maryland’s Commission has on reducing the prices for hospital services, which continues to be a significant driver of healthcare costs here in California. The Maryland model sets prices for hospital services, and includes Federal payers, which is an important part of its success. For these reasons, we request consideration of proposals focusing the Commission’s authority to create price recommendations for medical providers and facilities; not secondary and tertiary service providers where medical care is not administered. Health insurance is expensive because health care is expensive, and this would provide regulation of the cost drivers.

3. Establish Equity and Quality Standards

Equality is Not Equity

While it has been asserted that a single payer approach to healthcare is the only path to equity, we caution that equality should not be confused for equity. Meaning that although a one-size-fits-all approach, like single payer may provide all Californians with a single “equal” option for healthcare coverage, that should not be misunderstood to produce equal outcomes. Since one of the commendable objectives of this Commission is healthcare equity, we encourage support of health plans with cultural competence and an appreciation for the uniqueness and diversity throughout California.

An example of an existing health plan that serves regional needs is Chinese Community Health Insurance Coverage (CCHP) which is a non-profit plan option for people in the Bay Area offered through Covered California. CCHP’s enrollees receive a robust offering of personalized services in a way that is culturally competent and linguistically appropriate and with 60%+ of members identifying themselves as Chinese, this plan demonstrates an effective targeted model.

As earlier illustrated in Figure 1, many Californians that are uninsured already qualify for healthcare that they are not utilizing. Targeted communication to uninsured individuals is key to achieving universal coverage and equity in access and outcomes. Simply handing someone an insurance card does not translate to equity. The healthcare that the card represents must be meaningful to the covered individual or the impact will never be realized. There are numerous plans that are currently offered both on and off the exchange whose purpose is the promotion of high-quality health care that reflects cultural diversity with respect and competence. Specialized healthcare services such as Indian Health Service and plans such as Molina, CCHP, LA Care and others, embrace and reflect diversity in ways that are making meaningful improvements in the communities they serve.

In the Fall of 2021 ,Covered California announced the proposed premium rates for 2022 and in a sign of market strength, yet another health plan joined the California exchange, and some existing plans expanded their service areas. Every Californian will have at least two health plans to choose from, and a vast majority will have four or more plans to choose from. This is significant because when consumers have options, it drives health plans to keep costs down. Alternatively, market consolidation does not reduce costs, despite “reduced overhead;” rather, condensed, or single market monopolies produce inadequate benefits at a high cost. Consider the recent examples of the DMV, EDD and PG&E.

Social Determinants of Health (SDOH)

The disproportionate and tragic impact COVID-19 and natural disasters have had on the most vulnerable populations demonstrates that health insurance for all falls way short of guaranteeing health equity for all. Resources that enhance quality of life can have a significant influence on population health outcomes. We know that poverty limits access to healthy foods and safe neighborhoods, and we know more education is a predictor of better health. Differences in health are striking in communities with poor SDOH such as unstable housing, low income, unsafe neighborhoods, or substandard education. By applying what we know about SDOH, we can not only improve individual and population health but also advance health equity. Access to transportation, a warm meal and maybe someone with a friendly ear is good healthcare.

Our members know that health insurance is only one dimension of a person’s healthcare needs. We know that addressing SDOH has the potential to lower healthcare costs, while improving health outcomes for everyone. Accordingly, we encourage the Commission to discuss health insurance as one component of whole-person care, it cannot improve outcomes in a vacuum.

4. Demonstrate Pharmaceutical Cost Savings

Reduce the Cost of Healthcare by Reducing the Cost of Prescription Drugs

Of nearly 200 countries in the world, the United States is one of only two that allow direct-to-consumer advertising on pharmaceuticals. A Kaiser Family Foundation analysis of data from the Centers for Medicare and Medicaid Services and Truven Health Analytics shows that drugs account for 10% of U.S. health spending and represents 19% of the cost of employer insurance benefits. Celebrity endorsements or rose-colored commercials can lead to patient requests for costly medications influencing prescriber behavior. The proliferation of name-brand drugs is costly and troubling when other less expensive alternatives are available and effective.

Given the significant percentage of healthcare spending that prescription drugs account for, CAHIP supports additional efforts to build on the momentum of California reforms chaptered in 2017. Those reform bills include AB 265 (Wood), which prohibited drug manufacturers from offering coupons for pharmaceutical drugs when other FDA-approved drugs are available and less expensive. Additionally, transformative regulation came from SB 17 (Hernandez), which improved transparency in the health care system by requiring drug manufacturers to give prior notice to purchasers before raising prices and required additional data submission on costly and frequently prescribed drugs.

We would encourage the Commission to petition the Food and Drug Administration to not allow direct consumer advertisements, particularly TV or radio commercials, for prescription drugs. Commercials have numbed consumers to side-effects as serious as death, and according to Dartmouth College, has done so to the tune of $30 billion annually. The idea to ban pharmaceutical ads is not new and has been supported by the American Medical Association since 2015. “(Support for) an advertising ban reflects concerns among physicians about the negative impact of commercially-driven promotions, and the role that marketing costs play in fueling escalating drug prices,” said AMA Board Chair-elect Patrice A. Harris, M.D., M.A. “Direct-to-consumer advertising also inflates demand for new and more expensive drugs, even when these drugs may not be appropriate.”

5. Collect and Use Healthcare Payments Data

Address the Cost of Health Care with Price Transparency

Health insurance is expensive because healthcare is expensive. To address the root causes of affordability, CAHIP recommends strong enforcement of existing federal government orders for hospitals to publish prices. The New York Times recently published an article that highlighted abuses in plan and hospital negotiations and billing practices. Some examples are as egregious as charging lower costs to people who forgo insurance all-together, which undermines the objective that insurance is for the consumer’s benefit.

Without comprehendible price transparency, it is impossible for consumers to choose the coverage that is right for them. Employers and individuals may be choosing a premium that is “right” for them without any ability to confirm that the applied coverage is working to their benefit. Charges need to be consistent, predictable, and transparent. In addition to the alternative pricing models discussed earlier, CAHIP recommends stronger penalties for failed compliance with existing federal price posting requirements. Existing penalties are capped at $109,500 per hospital, per year, so financially perverse incentives presently outweigh the punishment. Further, the published data should be in a format that is transparent to consumers and their agents to ensure that coverage is selected based not just on premium affordability, but on healthcare affordability.

6. Build expanded, Culturally Sensitive Workforce

Providing insurance to all Californians is an important milestone, however for that coverage to be fully realized we must also increase the number of providers who are available to provide care. We are confident that other stakeholders more closely aligned with patient treatment will be able to comment on ways to increase the number of providers our state desperately needs.

Ask an Agent

Agents are present in virtually all communities of our state, including in over 500 Covered California storefronts. Agents also reflect the diversity of our state with nearly three out of five agents speaking more than one language. Some 11,000 agents’ contract with Covered California and are required to meet a stringent certification process that includes the obligation to help consumers find the health plan and coverage that is best for the consumer and commit to serving ALL Californians, regardless of their age, disability, race, ethnicity sexual orientation or gender identity or ability to pay.

Agents are playing a vital role in making sure Californians are aware of the additional premium assistance made available by the American Rescue Plan offered through the entire 2022 coverage year. This additional coverage will largely absorb the nominal average expected premium rate increase of 1.8 percent on and off the exchange. Further, consumers that use agents to shop and switch can see premium reductions. Using an agent’s professional advocacy costs consumers nothing additional.

Agents are available to help people sign up for the coverage that is right for them, their families, and businesses. They also provide the ongoing service and support necessary for individuals to effectively utilize their healthcare coverage. Agents assist with group coverage, Medicare, no-cost Medi-Cal, and Covered California plans; some with premiums as low as $1 per month for individuals that received unemployment assistance. Additionally, agents were a cornerstone of ensuring that all Californians were able to maintain coverage throughout the unprecedented COVID-19 pandemic, when coverage and an advocate have never been more essential.

These men and women are trained and licensed professionals who operate diverse storefronts throughout California and offer in-person and remote enrollments and consumer advocacy services. Their expertise is increasingly important to consumers because they make complex issues understandable. Agents often reflect the diversity of their communities and serve as the friendly face for what can otherwise feel like an intimidating and cold government/corporate transactional mandate. Health insurance agents bring the irreplaceable human touch necessary to providing a true quality service experience to their individual and employer-based insurance clients.

Conclusion

While CAHIP ardently agrees with the objective of containing costs, improving quality, and reducing disparities, we respectfully caution against unintended consequences of harmful cuts to services and decreased access that would likely occur if related legislation is drafted in error. CAHIP is available to discuss options to help to repair problems encountered by Californians who are trying to obtain and pay for health insurance coverage. Thank you for the opportunity to provide feedback on this final report. We appreciate the partnership in helping Californians get the coverage and care that is right for them.

|